Ireland just published ambitious plans to introduce automatic enrolment (AE) in retirement plans from 2024 onwards and since I always back AE as the single most important policy that can help people save for retirement, it’s well worth to look at the details, which are quite interesting and some came with some surprise for me.

According to the detailed plans published by the Ministry for social protection Ireland plans to have AE and all of the supportive systems up and running by the end of 2023 and ready to take first enrolments from early 2024 onwards. All employees aged between 23 and 60, earning over €20,000 per annum (across all employments), which are not already contributing to an occupational pension plan, will be automatically enrolled. They will be free to opt-out at the end of the minimum membership period during the 7th and 8th month and on each occasion during the first ten-year period in which contribution rates will increase. Those who opt-out will also be automatically re-enrolled after two years (smart feature).

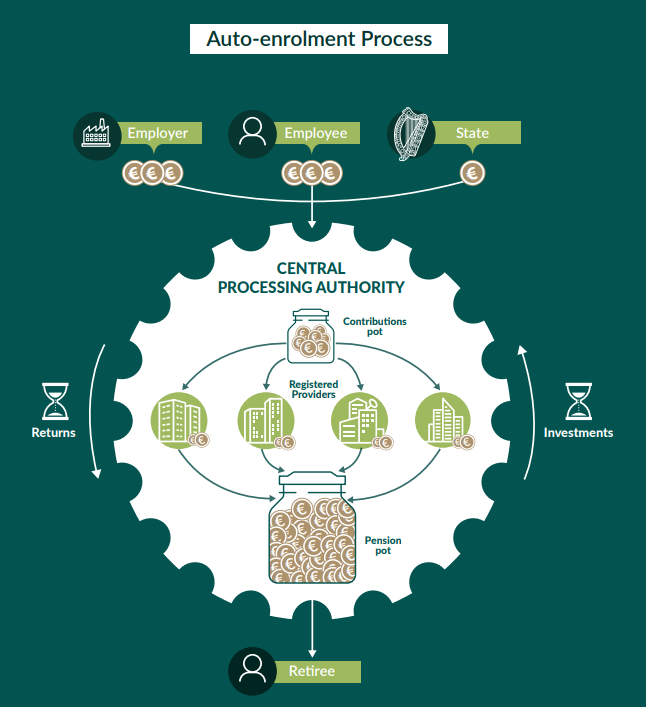

Once employees are enrolled they will have to make their own minimum contributions as well as receiving 100% matching contributions from their employers and an additional top up from the state. In the first 3 years employees and employers will each contribute 1,5% of a person’s gross earnings and the state will top this with an additional 0,5%. This means for each €1 saved by an employee, €2.33 will go to their savings account (Employee €1 + Employer €1 + State €0.33). The smart thing here is, that similar as in the UK, minimum contributions will increase over time every 3 years until they reach 6% after 10 years. From that point on the minimum contributions will be 6% employee, 6% employer and 2% from the state, which is quite ambitious and rightly so, as we all know that we need sufficient levels of contributions to ensure adequate retirement pots. So again one really positive feature. Employer contributions will also be deductible for corporate tax purposes.

Investment choices

Regarding investment choices all members will be able to choose from a range of four funds:

- conservative fund (mainly government bonds, cash, or cash equivalents)

- moderate risk fund (government bonds + blue-chip equities, stock exchange indices, …)

- higher risk fund (equities and real estate)

- special default fund which will operate on a life-cycle principle, meaning having more equity investments at the start and then reducing this to lower risk investments as the member nears retirement.

From behavioral economics and decades of experience we now know that most members will be enrolled in the default fund and they will not make any investment choices on their own. In Slovenia all members of retirement plans choose at the start one of the three life cycle funds we have on offer and the vast majority does not make any active choice and are enrolled in the fund according to their age, meaning the younger members go in the equity fund and the older to the guaranteed fund.

What is interesting and specific about Ireland’s plans is that the funds will be provided by four commercial investment managers that will be selected through an open tender, and each provider will be required to offer all four funds. All contributions to a particular fund type will be pooled and distributed between the providers and also all returns will be pooled, which means all employees in the same fund type will receive the same return. Quite an interesting solution, I have to say. Also annual management fees will be capped at 0.5% of assets under management. Also interesting, employees are to have no direct contact or relationship with the investment managers. This will also, according to the ministry, minimise the administrative burden for employers, as they will not have to select any provider and will only have to make payroll deductions of contributions. I would add this also means employers will not have any fiduciary duty and be liable for the selection of providers. This also presents a certain departure from the existing system of occupational pension plans in Ireland, so this solutions comes as quite a surprise for me.

The state plans to establish a special “central processing authority (CPA)” as they call it, that will be the single point of contact for the members. All members will be able to access their account information directly with the central processing authority that will also enable the so-called ‘pot-follows-member’ approach meaning portability of pension pots will not be an issue. The CPA will also contract a small number of commercial auto-enrolment providers to offer a range of savings/investment products and it will facilitate the collection of the employee and employer contributions and the State ‘top-ups’ as well as distribute funds to members when they reach retirement age.

Modified from: Department of Social Protection (https://assets.gov.ie/219768/4aada71d-2731-4522-b218-9184a699652f.pdf)

Decumulation options

Once members reach retirement they can start to drawdown their savings (this is currently at age 66). Drawdown of the pension pots is possible by using the existing range of regulated pension products (lump sum (subject to regulated limits), annuity or an ARF – Approved Retirement Fund) and members can engage with existing commercial providers on the market. If the need would arise, the Central Processing Authority mentioned before might select by tender a set of pension drawdown products.

The impact of AE

According to the Department of Social Protection approximately 750,000 workers will be enrolled into the new scheme. In total, the new system will, according to state estimates, generate €21 billion in funds under management over the next ten years excluding investment returns which is a sizable amount of assets for Ireland. Looking at the individual level, estimates from the state predict for an average worker earning €40,000 annually, the new system could generate in total after 43 years of saving a pension pot worth more than €560.000 including estimated investment returns. This is life changing amounts of assets that can have a dramatic positive effect on people’s lives in retirement and I will follow the implementation of the new AE system in Ireland with great interest.

References:

Department of Social Protection (2022). The Design Principles for Ireland’s Automatic Enrolment Retirement Savings System. Retrieved from: https://assets.gov.ie/219768/4aada71d-2731-4522-b218-9184a699652f.pdf

One thought on “Ireland to introduce automatic enrolment in retirement plans”