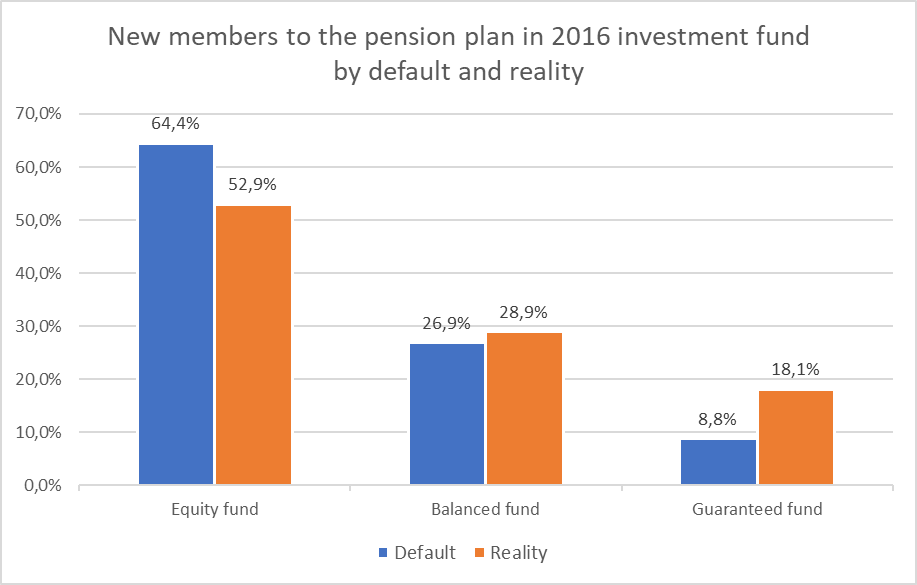

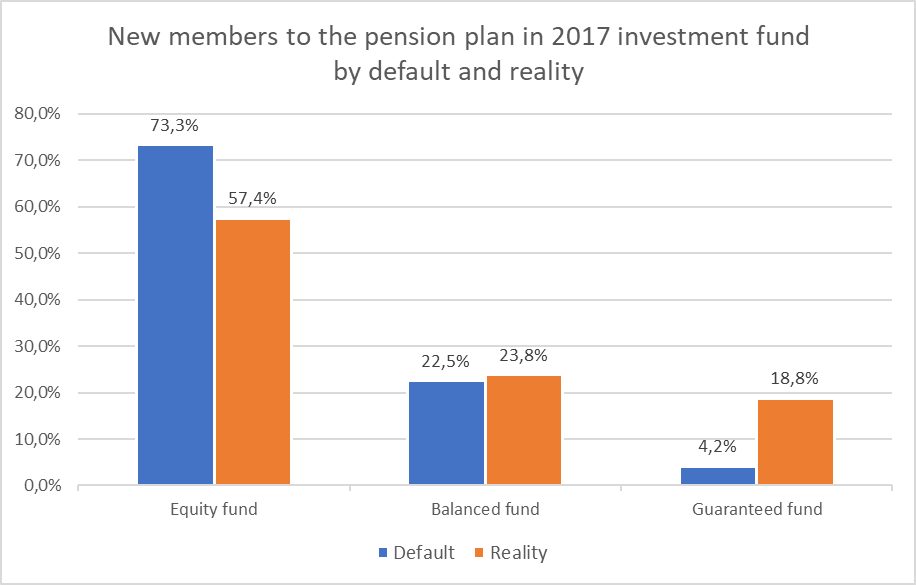

The other night, my 11-year-old son was on a mission. Eyes locked on the screen, fingers dancing over controls, he explained to me with the urgency of someone managing a high-stakes portfolio that he just needed “five more minutes” (his screentime is very limited) to reach 24,800 points and level up in his favorite game, Brawl Stars from Supercell. As I watched him strategize his every move, it struck me that, in many ways, his focus on small goals is exactly what’s missing in how we approach retirement savings.

Whether in Brawl Stars or life, having clear, achievable goals and immediate feedback keeps things interesting. In the retirement saving game, however, the “prize” feels distant decades into the future, abstract, and—let’s face it—not always thrilling. But with the right approach, setting small, incremental goals can make a seemingly endless journey feel like an engaging quest where every step is worth celebrating. And as providers of pension plans, there’s a lot we can do to make that journey more compelling for our members.

Short-Term Goals: Making the Long Game Fun

Retirement saving is more marathon than sprint—a never-ending level with the finish line decades away. Without small goals along the way, it’s easy to feel like you’re running forever, with no sense of progress. My son’s strategy of reaching 24,800 points to level up is a perfect example of a goal that’s challenging yet achievable. Imagine if your retirement saving account had milestones, too—small, meaningful “levels” where you could see exactly how much progress you’ve made toward the big goal.

Small but achievable milestones in Brawl Stars

Source: screenshot from Brawl Stars

Pension providers can make this happen. By designing online accounts with set goals that are more tangible than “retirement”—say, hitting the next €10,000 mark—members would have benchmarks they can celebrate along the way. And hey, the occasional badge or reward for reaching these milestones might just add some motivation (and even a bit of fun) to the process.

Keeping It Engaging: Rewards That Make a Difference

In Brawl Stars, every level-up comes with rewards—maybe it’s a power-up or a cool new character. The goal is simple: keep players engaged. In retirement planning, we could use a bit of that gamification. Imagine if every time you added another $5,000 to your account, you received a little bonus feature, or maybe even a notification celebrating your success. Small rewards for hitting each milestone could keep people interested, reinforcing the feeling of achievement as they reach each new level.

And here’s where we, as pension plan providers, could really get creative. Let’s bring in some of the best UX designers from the video game world (if we can pay them enough, of course). Let’s make tracking retirement savings feel as intuitive and visually engaging as tracking progress in a game, so that even the most financially wary member feels the thrill of seeing their balance climb.

Could the retirement saving account of the future look similar?

Source: screenshot from Brawl Stars

Scorekeeping: Knowing Exactly Where You Stand

In Brawl Stars, every point is tracked, every level-up recorded—players know precisely where they are and what’s needed to get to the next level. Retirement savers deserve the same clarity. With clear visual scoreboards showing how far they’ve come and what’s left to reach each goal, online accounts could show members exactly how close they are to the next reward or milestone. Having this transparency not only boosts engagement but also provides much-needed clarity for people wondering if they’re on track.

And while we’re at it, imagine if we sent out personalized notifications or “progress alerts” just like in games. “You’re only $2,000 away from hitting your next milestone!” or “Congratulations! You’re halfway to your target for this year!” Little boosts like these could go a long way in keeping people invested—literally and figuratively—in their retirement goals.

Let’s Hire Some UX Designers from the Video Game Industry

Let’s face it: if saving for retirement felt as satisfying as leveling up in a game, we’d probably all be more motivated savers. The video game industry has mastered the art of keeping players engaged and challenged. To make saving for retirement more like a real-life quest, why not borrow some ideas from the gaming world? Pension providers could design interfaces that are colorful, user-friendly, and dynamic (there are some bright examples also in the retirement industry, but a lot of us are just not there yet), with dashboards that display progress in a clear, gamified way. If hiring top-tier video game designers is the secret to better engagement, well, maybe it’s time to start recruiting—if we can convince them to trade game controllers for retirement calculators!

Future Potential: AI and Personalization in Gamified Retirement Planning

Gamification could become even more powerful when combined with AI. Imagine a future where personalized, data-driven goals are set based on each user’s financial habits, income changes, or spending patterns. AI could generate custom “levels” for each user, guiding them on small financial steps to boost retirement savings in a way that feels tailored and responsive to their unique journey.

Many savers also lack confidence in investing and retirement planning simply because they don’t understand it well. By using gamified tools that educate users about concepts (like risk tolerance or compounding interest) at different “levels,” providers could help demystify retirement planning and empower savers to make smarter decisions.

Leveling Up Your Future, One Goal at a Time

The next time saving for retirement feels like an overwhelming goal with no immediate payoff, remember: every quest, however big, starts with small, achievable steps. Just like my son’s determination to reach the next level in Brawl Stars, breaking down retirement saving into short-term goals can make a long journey feel rewarding at every turn and the providers of pension plans have a long way to go here and we need to step up our game.

But I’d be remiss if I didn’t mention one of the major roadblocks we face in the retirement planning industry: legacy back-office systems. As much as we’d like to bring in the gamified features and dynamic interfaces of today’s most popular apps, these older systems can make innovation challenging. They weren’t built for modern, user-focused experiences, and adding gamification often requires substantial overhauls which takes a lot of time and money. Still, there is no excuse for poor UX even in the retirement industry (something I say quite often in the office) and we will all have to put in the needed hours and euros or dollars to “level up” —one goal, one milestone, one reward at a time. And maybe one day, saving for retirement will feel as exciting as reaching those 24,800 points to reach the next level in a game.