Ever wondered why many restaurants feature lobster or other expensive dishes at the top of their menus? Well one thing is for sure, it’s not a coincidence and the main function of the lobster is not for you to order it but to make other dishes look less expensive. Let me explain.

Anchoring is one of the more well-known behavioural biases in finance and also many seasoned marketers are well aware of it. Anchoring is a form of priming effect whereby initial exposure to a number serves as a reference point or anchor that influences all our later decisions. If that sounded too complicated here is a short example. If you go to a coffee shop and see first on the menu a $4,65 Cinnamon Dolce Latte this serves as an anchor to which you compare prices of all other beverages and all of a sudden that $3,45 Caffee Latte looks like a real bargain. But what would happen if you would not see the initial high anchor of the Cinnamon Dolce Latte, would you still perceive the $3,45 Caffe Latte as a bargain? Probably not. This is why nowadays many bars and restaurants turn the design of their menus in real science and you can read more about it here. Also providers of other goods and services, from mobile operators to tourist agencies, use anchoring extensively to sell us more.

But since I write about retirement saving let’s look at anchoring in finance. Nobel laureate Robert Shiller was one of the first to study anchoring in stock exchange trading and found investors are often anchored on the purchase prices of shares that serve as a psychological benchmark for future investment decisions [1]. The anchor price carries a disproportionately high weight in an investors decision-making process and often leads to bad investment outcomes. For example, if you purchased Tesla shares this august for $300, then this price will serve as an anchor for all future sales or purchases of this stock, regardless of how the stock actually performs and how Tesla is operating in reality. All future trades will always be measured to the $300 anchor. Because of this investors tend to hold investments that have lost value, because they hope they will return to the purchase price and by that they are taking on greater risk and blindly chase the purchase price, sometimes even to zero.

We judge other financial products in a similar way, and if I had the last deposit at a 3% interest rate, I am very disappointed with the deposit offer today, as I still judge all current offers by how much they are lower or higher than the last offer I got. The fact the interest rates plummeted to zero or even negative doesn’t change my sentiment as the anchor effect still follows me.

Can anchoring also hurt my retirement nest egg?

Unfortunately in many ways. One thing professor Shiller also found out was that besides the so-called quantitative anchoring, which is related to numerical values, we are also influenced by moral anchors which is the influence of intuition and emotions. A nice example of moral anchoring is investing pension savings in shares of the company where you are employed. This is very common in the US, where even today more than half of employees have most of their retirement savings invested in shares of the company where they work and you don’t need a Nobel prize in economics to figure out this is not wise. Shlomo Benartzi and Richard Thaler wrote back in 2007 about employees investing retirement savings in their employer’s stock as an example of poor diversification [2]. This occurs because we feel, when investing in shares of companies where we work, a false sense of security, as we feel we know the company more than others and because of this, we perceive it as a safer investment. Because of moral anchoring a plant worker employed by Ford, will much rather invest his retirement savings in Ford shares than BMW shares or even a diversified portfolio of shares. By doing this employees take on too much risk, as if something goes wrong with the company where they work, they will not only lose their job, but also their retirement savings. Not to mention investing in only one share is far far more risky than investing in a diversified portfolio.

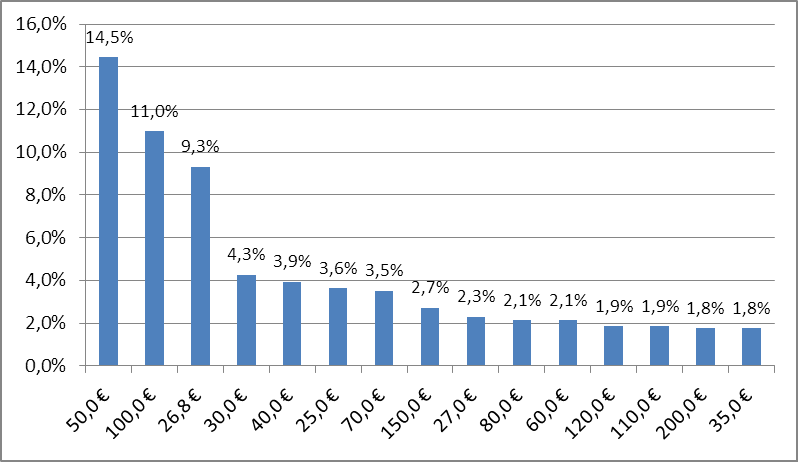

Anchoring also has a big effect on contribution rates of retirement plans as employees often anchor on the maximum rate matched by the employer, the maximum rate allowed by the plan, or a round number. So for example, if the employer matches contributions up to 4% of employees salary, most employees will also contribute 4%. I see the same pattern in the corporate pension plans we manage in the pension fund I work in Slovenia (Pokojninska družba A) where we manage more than 200 corporate plans and in the plans with an employer match most employees contribute the same amount. To test if individuals are also influenced by anchoring I conducted an empirical analysis of contribution rates of our individual pension plan a few years ago. The analysis included four years of data (N = 5,678) and revealed members chose monthly contributions that were round numbers and multiples of five far more frequently than would be expected by chance. Two levels of contributions in particular (€50 and €100) stood out. The analysis also revealed the power of anchoring as the plan’s minimum monthly contribution of €26.8, which is stated on the entry form, was also among the most frequent contributions. You can read more details about the analysis and round number bias in my article for the Behavioral Scientist Magazine [3].

15 most frequent monthly contributions to the individual pension plan of Pokojninska družba A in 2015. Members who chose annual contribution were excluded as the focus was on monthly levels only.

Minimum contributions will not be enough

Anchoring on the minimum level of contributions is really dangerous as they will just not suffice to build up a big enough retirement nest egg to provide sufficient income in retirement. One quick fix we did in our pension fund right after my analysis, we eliminated from the entry form the caveat where minimum monthly contributions were stated and we designed a special mobile app and web calculator that enabled potential members to calculate how much they should contribute in order to accumulate sufficient assets. This way we established a connection between the level of contributions members pay, to the amount of income they can expect to receive once retired and this gave them a better indication of how much they should contribute and steered them away from anchoring to the minimum amount.

Defaults to the rescue

Voya Financial, a provider of retirement products in the US where professor Shlomo Benartzi also works as an academic advisor for their Behavioral Finance Institute, experimented with pushing up default contribution rates in their retirement plans and found out pushing default contribution rates on the high side is less likely to generate unintended consequences than erring on the low side. This means, it absolutely makes sense for default rates of corporate plans to be as high as possible and go even into double digits, as they do not scare off employees from saving. More details on how defaults can be used to increase retirement saving in a working paper by Beshears, John et al [4].

One also very effective way of getting members off their default contribution rates is automatic escalation of contributions which is quite an old idea, but one still not explored enough. This way contributions rise automatically every year and even if I start with a low level they will be, effortlessly and without any decisions and cognitive effort from me, increase over time to an appropriate level. When mandatory automatic enrollment in corporate retirement plans was introduced in the UK a few years ago it featured a smart policy of automatically increasing contribution rates over time and it worked marvelously as research from NEST Insight shows the increases had no material impact on members and the proportion of members ceasing payments because of it was minimal.

Defaults can also help against moral anchoring on company stocks mentioned before and retirement plans should have diversified life cycle funds as the default investment choice and this way most members would be saved from investing in risky company stocks. The same can be used in the future to promote ESG investing that could be made the default option in corporate pension plans.

As we see, we can quite quickly and without even noticing it anchor ourselves into bad choices and they can in the end cost us much more than juts paying for that over priced Cinnamon Dolce Latte. Hopefully the retirement industry will be, with the rise of smart decision tools like retirement calculators, advanced online accounts incorporating robo-advisors and personalised recommendations, able to harness anchoring for positive reasons to help people save more for retirement and keep their savings invested in the right way. Until then, we need to be aware of its presence and not be tricked into ordering too many lobsters or overpriced coffee along the way.

References:

[1] Shiller, R. J.. Irrational exuberance. Princeton, NJ: Princeton University Press, 2015.

[2] Benartzi, Shlomo & Thaler, Richard. Heuristics and Biases in Retirement Savings Behavior. Journal of Economic Perspectives, 21 (3): 81-104, 2007. Retrieved from: https://www.researchgate.net/publication/4981794_Heuristics_and_Biases_in_Retirement_Savings_Behavior

[3] Vižintin, Žiga. Why Five and Not Eight? How Round Number Bias Can Reduce Your Nest Egg. The Behavioral Scientist. Retrieved from: https://behavioralscientist.org/five-not-eight-round-number-bias-can-reduce-nest-egg/

[4] Beshears, John and Benartzi, Shlomo and Mason, Richard and Milkman, Katherine L.. How Do Consumers Respond When Default Options Push the Envelope? 2017. Retrieved from : https://professionals.voya.com/stellent/public/6114876.pdf

One thought on “The dangers of anchoring in retirement saving”