Psychological inertia is best described as a general tendency towards inaction and because actions are always associated with some mental or physical effort, we prefer to avoid it and maintain the status-quo. Inertia is just one of the behavioral reasons millions all across the globe are still not saving for retirement and for the ones who are already saving it can have a big influence on their contribution rates and investment allocation, and the purpose of this article is to share one bit of novel research regarding the influence of defaults on investment allocation of pension plan members.

Luckily behavioral scientists like Brigitte Madrian, James Choi, David Laibson, Shlomo Benartzi and Richard Thaler, just to name a few, found a way to use inertia in a positive way to help people save for retirement by the use of “automatic enrollment”. Under automatic enrollment all employees of a certain company are enrolled in the pension plan and given an option to opt-out if they do not wish to participate. You can read more about the success of automatic enrollment and its evolution in my article from last december. What is also an integral part of any auto-enrollment is the default contribution rate and investment policy, which is in most cases set by the employer or it can also be set by the government depending on a particular policy. Because of defaults the employee doest have to make any choices regarding how much he or she will contribute and where the contributions will be invested. There has been quite a lot of research and lately also meta-analysis on how and where defaults influence decisions and you can find some of them in the references at the end of the article.

In 2016 pension funds in Slovenia could start offering life cycle funds and members now had a choice between three investment funds which were limited by age (before members had no choice and were enrolled in guaranteed funds). The younger members could start saving in high equity exposure funds, when they reach “middle age” they are automatically switched to medium equity exposure funds and before retirement they are again switched to the more conservative guaranteed funds with majority bond allocation and principal protection. By law each provider had to designate the maximum age limits when members must be switched from more dynamic to more conservative funds. This also means in practice that younger members have a choice between 3 funds, middle aged between 2 funds and older members have no investment choice and can only invest in the guaranteed fund. The legislation also prescribed how new members are enrolled in the funds, and all new members to the pension plans have to receive by registered mail a formal notice one month prior to their first contribution. The notice has to explain in plain language that they will be enrolled in the plan by their employer and give them the basic conditions of the plan. Members also have to receive a special investment fund selection form by which they select one of the three life cycle funds from their provider. What is also pointed out to members is, that if they do not send back the investment fund selection form within 10 days from receiving it, they will be enrolled in the fund according to their age. So what does the data tell us and how many members stick with the default?

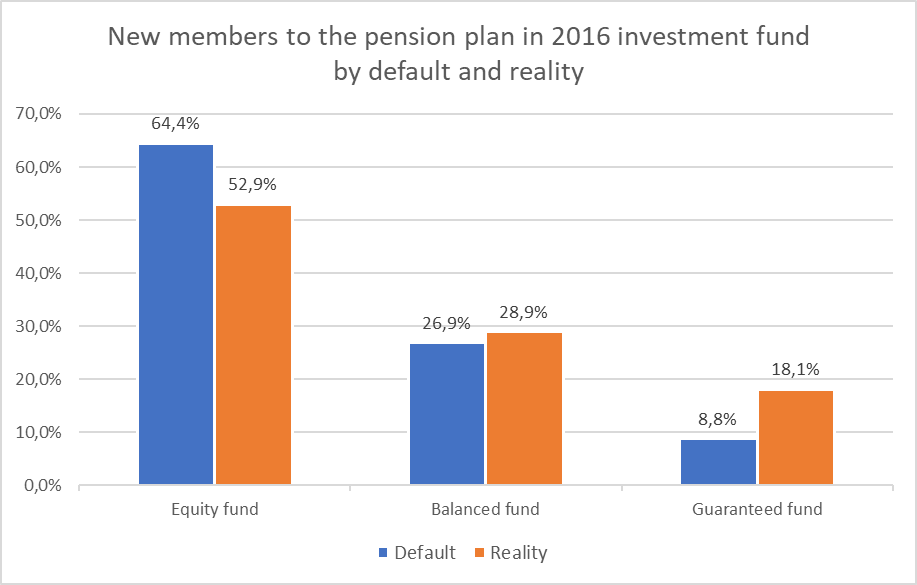

The data below is based on two years of data from members that joined the Pokojninska družba A, Inc. collective life cycle pension plan. The data contains only investment allocation of new members that joined in the years 2016 and 2017 (N = 5.953). In this particular pension plan the age limits for the funds are as follows: Equity fund is for members up to and including 42 years of age, Balanced fund is for members older than 42 years up to and including 55 years, and the Guaranteed fund is for members above 55 years. Members can also select a more conservative fund, meaning a member age 40 can go directly in the Balanced or Guaranteed fund. If all new members in 2016 (3.594) would stick with the default fund according to their age 64,4 % would be in the Equity fund, 26,9 % in the Balanced fund and only 8,8 % would be in the Guaranteed fund (marked blue on the chart).

So what was the actual fund selection of newly joined members in 2016 – 52,9 % joined the equity fund, 28,9 % the Balanced fund and 18,1 % the Guaranteed fund (marked orange on the chart). The data tells us the majority of members stuck with the default fund (chart below), but what we can also see is that 11,4 % of the members that would by age fall in the equity fund made an active choice and choose deliberately a more conservative fund with some of them choosing the Balanced fund and even more choosing the Guaranteed fund. This is why the actual membership in the guaranteed fund was at the end of 2016 18,1 % of all new members, if all would stick with the default the share would be 8,8 %.

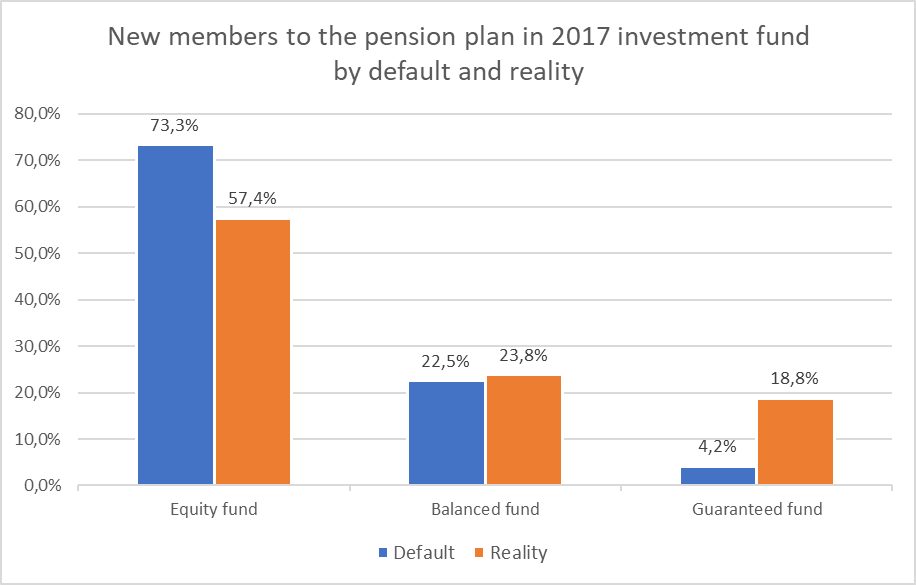

The data for new members in 2017 tells a similar story and again from all new members (2.359) the majority stuck with the default and 15,9 % made an active choice and chose a more conservative fund, which is evident from the chart below, again most of them going to the guaranteed fund.

Given all the literature I read on defaults in asset allocation of retirement plan members the results came as no surprise, as the majority of studies find strong evidence they work in similar circumstances. Members of pension plans who are automatically enrolled in the plans also have notoriously low levels of engagement and investment funds and wealth management are subjects not listed highly to be of much interest to the average employee.

One driver reinforcing the default in this case is also, that the default fund selection can in this context be perceived as being endorsed as the “right” option by the designers of the system – in this case the pension fund and also the Ministry of labour which was responsible for the legislation or even the employer that selected the pension plan provider. According to The Behavioural Insights Team report this effect is stronger where the trust in the system designer is higher, so if people trust the government or their employer or the pension plan, surely they must think that they have all thoroughly studied the issue of fund selection and their default setting according to the age of the member must be optimal, so why go against it. This effect is even more relevant in cases where individuals have limited knowledge on the matter, which fits this particular case again nicely.

What would be perfect of course would be, to have another collective pension plan with the same investment choices but no default fund allocation, as this would enable us to make a direct comparison and really establish the power of defaults in the case of investment fund selection. Here in my opinion, how the fund selection options would be framed would have a big influence on the end decisions – for example Balanced fund (appropriate for members up to and including 55 years of age), or Balanced fund (suitable for members aged 42 to 55 years), etc. – and also what other data would be presented to members on the selection form, like the last five annual yields of each fund, in this case the actual yields would influence members decisions even though as the old saying goes, past performance is no guarantee of future performance. You can read more about the dangers of anchoring when it comes to retirement saving in my article from 2020.

Defaults can have a big influence on where pension plan members invest their contributions, so this is why it is super important to get them right, meaning members should be defaulted in carefully selected investment options, whether it be life cycle or target date funds, balanced funds, managed accounts, … with proper asset mix, low transparent fees and good governance. Because defaults work that good the people designing them must pay extra attention, so the outcomes are in the end really beneficial to the members. There is also an increasing debate about defaults when it comes to decumulating retirement assets and some also propose alternatives to the investment phase defaults, which are for the time being dominated by target date funds, but this is a topic for a different post. For the time being, when it comes to defaults of investment options in pension plans, they seem to work in the presented context, so we better get them right.

References and further reading:

[1] The Behavioural Insights Team (2021). A rapid evidence review from the Behavioural Insights Team for the Pensions Dashboards Programme. Retrieved from: https://www.pensionsdashboardsprogramme.org.uk/wp-content/uploads/2021/06/BIT_PDP_REA_01-06-21.pdf

[2] John Beshears, James J. Choi, David Laibson, and Brigitte C. Madrian (2006). The Importance of Default Options for Retirement Savings Outcomes: Evidence from the United States. NBER Working Paper No. 12009. January 2006, Revised March 2007. Retrieved from: https://www.nber.org/system/files/working_papers/w12009/w12009.pdf

[3] JACHIMOWICZ, J., DUNCAN, S., WEBER, E., & JOHNSON, E. (2019). When and why defaults influence decisions: A meta-analysis of default effects. Behavioural Public Policy, 3(2), 159-186. doi:10.1017/bpp.2018.43

[4] ZHAO Ning, LIU Xin, LI Shu, ZHENG Rui (2022). Nudging effect of default options: A meta-analysis[J]. Advances in Psychological Science, 2022, 30(6): 1230-1241. Retrieved from: https://journal.psych.ac.cn/xlkxjz/EN/Y2022/V30/I6/1230

[5] Pablo Antolin, Stéphanie Payet, and Juan Yermo (2010). Assessing default investment strategies in defined contribution pension plans. OECD working paper on finance, insurance and private pensions. Retrieved from: https://www.oecd.org/finance/private-pensions/45390367.pdf