Automatic enrolment (AE) in retirement plans is far from a new idea, in fact it’s now more than two decades old, but I’m still surprised how many people in the industry (finance, insurance, retirement, …) and also in the government, are not aware of how powerful it really is. Every time the debate in my home country of Slovenia comes to the second pension pillar and how to increase enrollment rates, I mention AE as being the no-brainer solution, but it is always received with scepticism. Also at international panels, pondering on how to get people to save for retirement, there isn’t a general consensus that this is “the solution” and we always end up with general remarks like, we need more financial education and raise awareness, we need to increase tax incentives, yada yada yada.

So in light of the new fascinating numbers the UKs Department for work and pension (DWP) has just released – more than 10 million people saving thanks to AE in the UK and a great overview just published – Best practises and performance of auto-enrolment mechanisms for pension savings [1], I think it’s the right time to make the case again for AE in retirement plans and see how the idea went from concept to reality in the last 20 years and what are the latest best practices to make AE a success.

How does it work?

We know from lots of behavioural science literature the initial decision to join a retirement saving plan is one of the hardest. There are numerous behavioural biases working against it, from loss aversion to status quo bias and many more. While seeking an alternative way of how to get people over this hard decision researchers like Brigitte Madrian, James Choi, David Laibson and not to forget Shlomo Benartzi and Richard Thaler with their breakthrough Save more tomorrow program, made the case of how to use inertia to help people save for retirement. They turned the concept around and instead of trying to convince people to join a pension plan with all kinds of awareness campaigns, tax incentives, … , they turned things around and proposed to auto-enrol all employees in the pension plan and to just give them the option to opt-out.

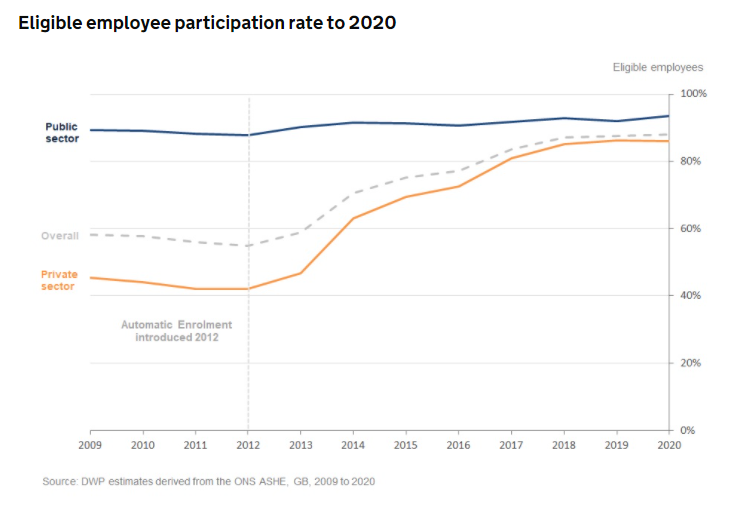

This way the participation in the retirement plan is still voluntary and everybody has the right to say no. There is just one crucial detail, saying yes and enrolling in the plan requires no effort and the only time you need to make any effort is if you want to exit the plan. What kind of an effect this can have on enrollment rates is more than obvious from the chart below from UKs DWP showing how AE in the UK raised participation in retirement plans. You need to be looking at the orange line representing participation of private sector employees in retirement plans and after 2012 when AE was introduced the effect is obvious.

What a stroke of genius AE is and I still remember reading the first time about this concept, as I was just blown away by its simplicity. Also the employee doesn’t have to make any hard decisions before joining the plan, like how much to contribute and in which fund to invest, as every plan featuring AE has a predetermined default level of contributions and fund selection, which is in most cases a target date fund. This way starting to save for retirement is totally effortless.

How it started and how it’s going

The US was one of the front-runners of AE. It all started in 1998 by the Internal Revenue Service Revenue Ruling 98-30 which clarified that AE was permissible for new employees and this meant new employees could be automatically enrolled in their company’s 401(k) and their contributions automatically deducted from their pay. The Pension Protection Act that followed in 2006 helped to popularise the concept even further, but always kept it on a voluntary level, so today more than half of employers feature AE in their retirement plans. This also means many are still not covered by AE.

The United Kingdom followed later with the Pensions Act 2008 under which every employer had to enrol their staff into a workplace pension scheme and contribute towards it. A mandatory version of AE was phased in from 2012 onward. First it was mandatory for big companies, then medium and down to small. What was really smart about AE in the UK was that also the minimum level of contributions was auto-escalated from the initial 2% of employees gross salary, to 5% up to April 2019 and now 8%, of which the minimum level from the employer is 3%. Another great feature of the UK`s AE is that even if employees opt-out of the system, the employer will “re-enrol” them back into a scheme every three years. After 9 years AE in the UK is still going strong and even in the Covid-19 pandemic the opt-out rates remain low at only 9 to 10 percent. Overall 88% of eligible employees (19.4 million) were participating in a workplace pension in 2020 according to the latest Department for Work & Pensions statistics which is miles away from how things were just 10 years ago and today more than 10 million people started to save for retirement thanks to AE.

Ireland is following and plans to implement by 2023 a defined contribution AE system of supplementary pension savings for all employees between the ages of 23 and 60 who earn €20,000 or more. Auto enrolment will be phased-in and minimum mandatory contributions will be set at 1.5% of gross earnings and then increasing by 1.5% every three years until year 10, when they will reach 6%. The detailed legislation is still being drafted and initially it was planned to be in place by 2022, but was unfortunately pushed back to 2023 and fingers crossed it’s not pushed back again. More details on the plans in the report by Mercer.

As mentioned before AE never became mandatory in the US, but a growing number of US states, like California, Oregon, Illinois and the latest New York, decided to push ahead and started to implement state-facilitated retirement savings plans in which employees are automatically enrolled. Oregon’s plan OregonSaves began in 2017, Illinois in 2018 and California started its CalSavers at the end of 2018. You can find detailed data on how the existing state plans are growing on Massena Associates website which is regularly updated.

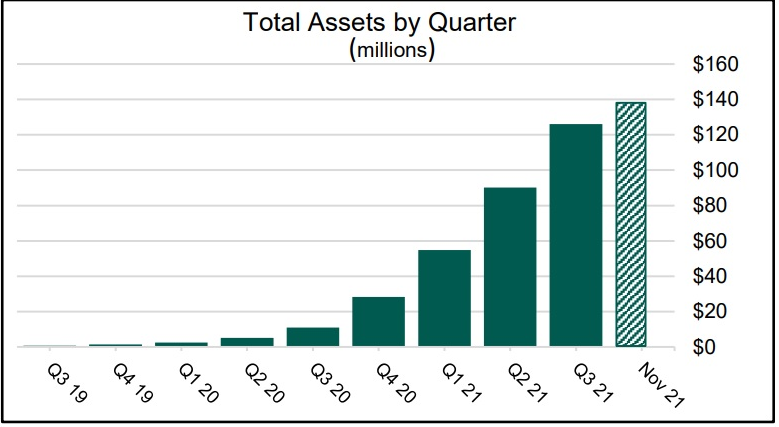

A nice example is CalSavers, which grew in just a few years to 209,033 funded accounts and 140 million USD assets by the end of november 2021, represented in the chart below.

Source: CalSavers Snapshot report november 2021, retrieved from: https://www.treasurer.ca.gov/calsavers/reports/participation/november2021.pdf

New York is the latest state announcing such a plan that will require certain employers to enrol their employees in a new state-managed retirement savings program funded by employees. The plan will be mandatory for all employers that had at least 10 NYS employees during the entire prior calendar year and have been in operation for at least two years and also don’t have a qualified retirement plan, like a 401(k). More on the latest NYS plan in the report from Willis Towers Watson.

In New Zealand, AE was introduced in the KiwiSaver Act 2006 and the KiwiSaver funds have been going strong ever since. Employers have to enrol their employers automatically and there is also a minimum rate of contributions for employers set at 3% of employee’s gross salary. Employees have a time limited option to opt out – only between 2–8 weeks of starting work. At the end of march 2021 members of KiwiSaver plans totaled 3 million and assets amounted to 81,6 billion USD according to the latest Financial Markets Authority report. KiwiSaver isn’t just a retirement savings plan, it can also help members buy their first home either through the ability to withdraw some of the savings or through a special First Home Grant. When buying your first home you can make a one-off withdrawal of most of your savings if you’ve been a member for at least three years. Opt-out rates remain low at around 15% making KiwiSaver a big success.

For a more detailed overview of AE in various countries I really recommend the report Best practises and performance of auto-enrolment mechanisms for pension savings by LE Europe, Redington and Spark written by Patrice Muller, Rohit Ladher, Shaan Devnani and Luke Pate.

How to make it work

The report mentioned above also nicely sums up some key recommendations for implementing AE schemes and how to make them work, from defining clear policy goals, establishing a wide consensus around both the goals of and the implementation, a supervisory framework empowering risk-based supervision of providers, phased introduction, and a nationwide information campaign ahead of the scheme’s introduction.

A clear best practice recommendation from the report is to provide mandatory access to occupational auto-enrolment pension schemes or in other words, to make it mandatory for employers to grant access to employees to an AE scheme. This feature is seen as a key feature that influences participation rates. Also recommended are: to have no waiting period (minimum tenure requirement) for employees to join AE schemes, to allow for automatic re-enrolment as in the UK example, to have mandatory employer contributions and to also cover self-employed workers. One feature also nicely executed in the UK was to raise the contribution levels over time making sure they are appropriate for the long term.

Regarding investment choices of members the recommendations are to have the presence of a default fund with capped cost, use of life-cycle funds and no joining fee and also to limit the number of investment funds per provider. Regarding decumulation, that is in recent times in developed private pension markets the number one topic, the report recommends to design the transition from accumulation to decumulation and to have a default option in place and not to force the members to make an active choice. According to the report, the default option for decumulation could consist of programmed withdrawals and a deferred life annuity for all but small savings balances and to have a free signposting service that would direct members to providers who could give them advice on decumulation options.

Trust is key

One important element nicely highlighted in the report as being a key component is trust. For AE to be introduced successfully, people must have trust in the system and if it does not exist, AE will not be successful and many people will use the option to opt out from such a scheme. So this crucial piece is sometimes forgotten and trust is something that can take years or decades to build, only to evaporate in days, so this issue is to be taken into consideration before introducing AE to a certain pension system. If there is no trust in the system itself, then even AE will not work.

To finish on the positive note, AE now has quite a strong and proven track record – given the right preconditions, and although it’s not the silver bullet solution to the retirement saving challenge, it comes very close and in my mind it’s the no brainer every country should implement in a way that best suits their existing retirement system taking into account the aforementioned best practices.

References:

[1] Best practises and performance of auto-enrolment mechanisms for pension savings (2021). Patrice Muller, Rohit Ladher, Shaan Devnani & Luke Pate. LE Europe, Redington and Spark. Retrieved from: https://op.europa.eu/en/publication-detail/-/publication/6f40c27b-5193-11ec-91ac-01aa75ed71a1/language-en

Well said; great stats Zig.

LikeLiked by 1 person