End of December Adam McKay’s new movie Don’t Look Up was released on Netflix bringing to us a fun satire of the current state of our society. An acclaimed cast, including Leonardo DiCaprio, Jennifer Lawrence, Jonah Hill, Meryl Streep and Cate Blanchett, show us thru a satiric lens, how our society is totally oblivious to the large challenges it is facing, which are in the movie represented by a large comet on a trajectory to Earth.

The story in the movie goes something like this. A PhD student named Kate Dibiasky (played by Jennifer Lawrence) discovers a comet and when she and her mentor Dr. Randall (played by Leonardo DiCaprio) calculate it’s headed straight for Earth bringing in six months a certain extinction of the human race, they go on a mission to save humanity. First they contact the government and get a meeting with the President of the United States (played by Meryl Streep) only to find out she does not take them even remotely seriously and is more concerned in getting re-elected than to start working on a plan to save humanity.

Being disappointed by the government they decide to risk it all and go to the media with their story and warn everybody. They tell their story to a newspaper and also go on a popular morning show called The Daily Rip, where again their warning of a certain apolicipse falls on deaf ears. They are made fun of and their calculations are being questioned, as it seems nobody wants to believe the harsh reality, even though it’s backed up by the most prominent scientists. Sounds familiar?

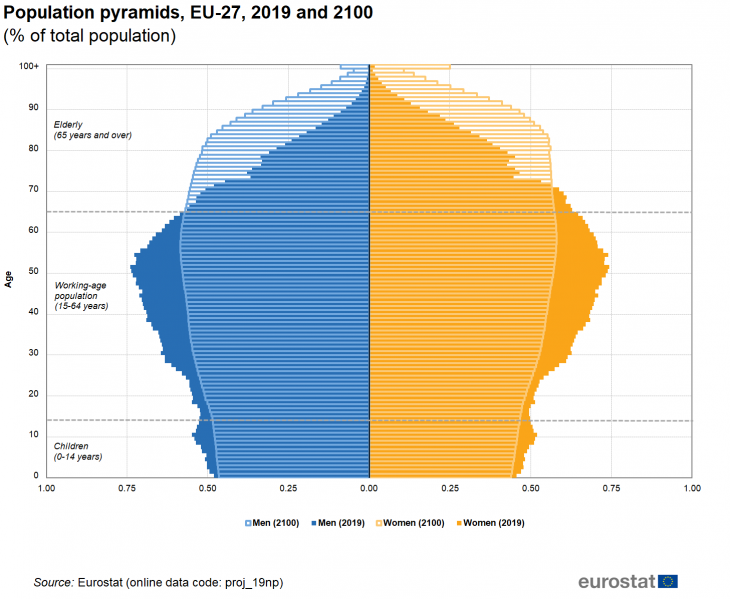

Initially Adam McKay wrote this movie with climate change in mind, but when I was watching the movie it immediately struck a parallel to our denial about the future demographic challenges we are facing. I remember my beginnings 10 years ago in the pension fund industry when I first started reviewing demographic projections, how the working age population will shrink in the European Union in the next decades, how the elderly population will increase and how we will live longer and longer bringing more and more strain on the public pension system. Until recently the population of most western countries were shaped like pyramids, with the larger young population cohorts at the bottom, smaller middle aged cohorts in the middle and at the top the smaller elderly cohorts. This meant the numbers of the working age population were much larger than the population of retirees and under these assumptions the modern day public PAYGO pension systems were devised. But what is happening recently and will play out in the future even more intensely is, the cohorts of the older generations are increasing relative to the younger ones meaning the population is no longer shaped like a pyramid, but more like a box. This transition is nicely seen from the picture below showing the population pyramids of European Union in 2019 and the projection for the year 2100.

Source: Eurostat (https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Population_pyramids,_EU-27,_1_January_2019_and_2100.png)

When you tell people that in the future, due to this demographic shift, public pension systems will no longer be able to sustain today’s levels of pensions guess what happens? Nobody cares and you can show all the excel charts and population pyramids in the world and people just shake their heads and move on with their daily lives, like nothing will happen, the same as it was in the movie. Nobody cared about the comet and nobody cares about the future challenges of public pension systems. The few of us who do are rarely taken seriously and to much disappointment, the same as in the movie, the political class is also all too often turning a blind eye to the demographic challenges, because the solutions are in most cases not popular – raising the retirement age and reducing the levels of public pensions. So politicians, who in most cases care only about getting reelected, are all too happy with delaying much needed reforms of the pension systems.

This is part of the reason why we are all too happy to live in denial when it comes to major challenges like global warming and the demographic shift and we are rather occupying ourselves with celebrity gossip and other “problems” of distant people. Meanwhile the comet is getting closer and closer. You can read more about the behavioral science of why we are bad at identifying and reacting to intangible and distant threats in my article from 2020.

Some things we can do to help people deal with intangible and distant threats is making them as personal as possible, so they feel it’s affecting them and their loved ones. Excel will not do the job here, so we need to break down the complex information into small bites and communicate it to people in plain language with no jargon and use graphics and imagery, so it’s understandable to a 5 year old. We can help people increase their emotional connection with the future self by using age-progressed digital avatars of themselves like Hal Hershfield suggests or use an age simulation suit that enables people to experience first hand all of the common impairments of older people, like I wrote in last year’s article.

We can learn a lot here from effective communication regarding the environmental challenges. Instead of only sounding the alarm horns of the impending doom the media and also everyone else should adopt a so-called solutions-oriented journalism which provides examples of how ordinary people are making a difference to big issues like climate change. It illustrates how those changes are having a tangible, positive impact on their lives. More on this novel approach in an article on The conversation.

The same can be applied to retirement saving, we need to show more concrete stories how additional retirement savings improved the lives of people and tell their stories and only then more people will be able to identify with them. In the pension fund I work for I saw first hand how this can work. In Slovenia private pension funds exist now for only 20 years and in the first few years there was lots of scepticism about it, people were asking will I ever get my money, and had similar concerns. In the last few years this has improved very much thanks to one simple reason, our first members were starting to retire and when they retire they also start to receive a lifetime monthly annuity from our pension fund. This had a dramatic influence on their perception as members were actually starting to receive the promised benefits and they shared this positive experience with their coworkers and this increased the positive attitudes of whole companies. We registered noticable change in positive attitude towards private pension saving in companies with high shares of ex-employees, who have already retired and started also to receive the private annuity from our fund and now we know those are our best promoters to increase positive attitudes towards additional retirement saving.

Here we need more interdisciplinary work and exchange of best practices from pension funds to environmental awareness campaigns, road and workplace safety and many other areas that all have one thing in common – addressing intangible and distant threats.

{kind=link}