While vacationing I try to catch up on my reading (as much as family life allows), and once in a while to take a break from more serious reading, I browse over my wife`s “lifestyle” magazines that she usually reads on the beach. Scanning over them this year, what struck me was how many articles were somehow related to ageing, or to be more precise, being and staying young. Just some of the titles that caught my eye: 5 exercises to keep you forever young, superfood for youth, Anti-ageing drinks, … not to mention many paid articles from cosmetic surgeons and other »beauty experts« promoting botox and other treatments to keep you young and firm.

What’s going on here, as these were not magazines for teenagers, but rather middle aged women and men. So it got me thinking – no wonder no one is interested in retirement saving, if all they are reading is eat papaya and drink carrot juice and you will be forever young. This disconnect or denial about ageing must for sure not be good as if I will be forever young, then why save for retirement or even think about it? I will rather spend all my money now on papaya and botox, forget about topping up my 401(k) retirement plan. Forget about saving for retirement at all, rather embrace the la dolce vita ideology and live the life.

This strengthens the already powerful present bias which has long been associated with undesirable spending and borrowing behavior. Present bias is the tendency of people to discount their future preferences in favor of more immediate gratification or to put it more simply, we are more inclined to spending and receiving short-term gratification – buying a new pair of shoes or that brand new Iphone, then to delay our gratification and save our paycheck and contribute to our retirement plan from which we will receive gratification only many years or sometimes even decades into the future. The concept was derived from the theory of self-control in behavioral finance back in 1981 by Thaler & Shefrin and you can find more details about it along with the latest research on this topic in an article by Jing Jian Xiao & Nilton Porto [1]. Their latest study also confirmed the theoretical predictions about the present bias, such as preferring to spend now and postpone saving.

What can we do about it? Xiao & Porto bring to light in their article an important role financial planners and other intermediaries can have in helping their clients be more patient and methodical when preparing long-term financial plans. Auto-enrollment saving programs can also in this case help tremendously to improve consumers’ financial well-being and get them to automatically contribute from their paycheck to their retirement plans and start building their nest egg, before they can spend it. The key element here being automatic payroll deduction of contributions to retirement plans before you get the chance to spend it. State-facilitated retirement savings plans in some US states like Oregon`s Oregon Saves and California`s CalSavers in which employees, who are currently not saving, are automatically enrolled in the new plans, are great examples of this. Not to forget auto-enrolment in workplace pension plans in the United Kingdom which has in less than 10 years increased coverage rates from 60 to 90 % and today more than 10 million people are saving additionally for their retirement because of it.

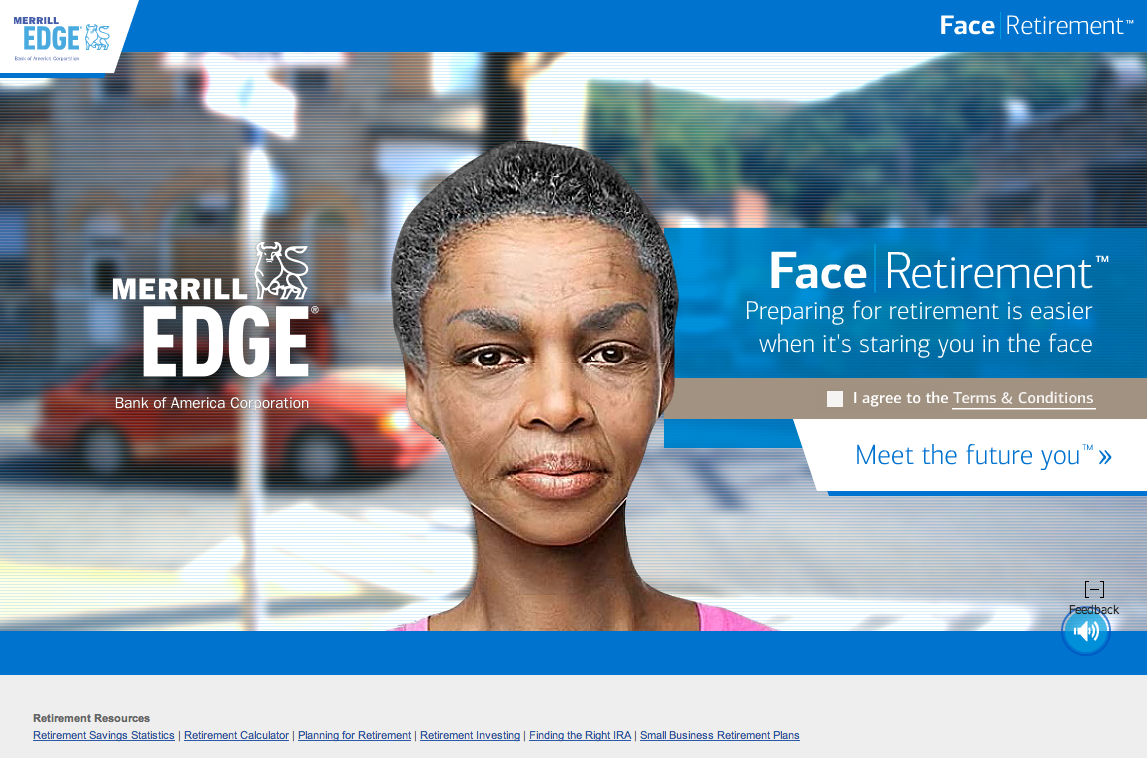

Hal Hershfield also has some interesting ideas to help people save for their future by increasing their emotional connection with the future self and as a result promote savings behavior. According to research, we consider our distant future selves, as if they are other people, and we of course don’t want to save our money for some stranger to spend in the future. To change this and increase our connection with our future self Hershfield experimented with using age-progressed computer renderings of people to see if that would increase the connection and help our saving efforts and it actually worked. In one experiment he used instead of age-progressed pictures only written and verbal exercises, like imagining or writing about your future self, and also that increased the connection with the future self [2]. He wrote many articles on this topic and they can be found on his website and I’m really looking forward to seeing more of his findings materialize in the future being integrated in features of retirement plans, for example using online retirement saving accounts with pictures of savers that could be aged. Bank of America Merrill Edge already integrated these features years ago with their Face Retirement App and you can check out the video on the link to see how it works.

Image source: https://charlotteultraswim.com/the-app-that-makes-your-face-old/

When I was thinking of how to bring the future to members of the pension fund where I work, to increase their connection with the future self, I stumbled online at GERT. The name is short for gerontologic simulator, which is best described as a sort of age simulation suit that enables you to experience first hand all of the common impairments of older people, like narrowing of the visual field, hearing loss, reduced grip ability, mobility restrictions, … you get the idea. Once you put it on even the most every day things become very hard, like sitting down at a desk and writing an email or walking down a flight of stairs and ordering a cup of coffee at a bar.

In the picture you can see me presenting the age suit at an HR conference and the suit was a great success and everyone wanted to try it. Personally the experience of wearing it was one of the most rewarding for me, as you experience first hand how tough it is to function in older age and my respect for older people grew to new heights, as it is incredible how tough life can be and before you feel it on your own you just can’t imagine it. The main purpose of the suit is to enable companies like retailers and banks to test their shops and branches and see how they cater to older people and to adapt them to become more friendly (at the link you can see how Barclays bank used it).

Our pension fund used the suite for a bit of a different purpose, which was to bring the future closer to our members and other people and to warn them about a not so distant future in which they will be in the shoes of today’s older people and how vital it is that we start preparing for the future today. That means living a healthy lifestyle to be more physically fit and also taking steps to secure a financially sound future, meaning putting some money aside today and not get lost in the la dolce vita ideology, as once we retire every penny will count and wearing the age simulation suit I’m even more sure we will need all we can get to make our retirement an enjoyable part of our lives.

References:

[1] Jing Jian Xiao & Nilton Porto (2019). Present bias and financial behavior. Financial Planning Review, Volume 2, Issue 2. Retrieved from: https://onlinelibrary.wiley.com/doi/full/10.1002/cfp2.1048

[2] Hal E. Hershfield, Elicia M. John & Joseph S. Reiff (2018). Using Vividness Interventions to Improve Financial Decision Making. Policy Insights from the Behavioral and Brain Sciences. 2018; 5(2):209-215. Retrieved from: https://irrationalretirement.com/wp-content/uploads/2021/09/cc3fc-hershfield_john_reiff_2018_pibbs.pdf

One thought on “The forever young ideology does not help retirement saving – what to do?”