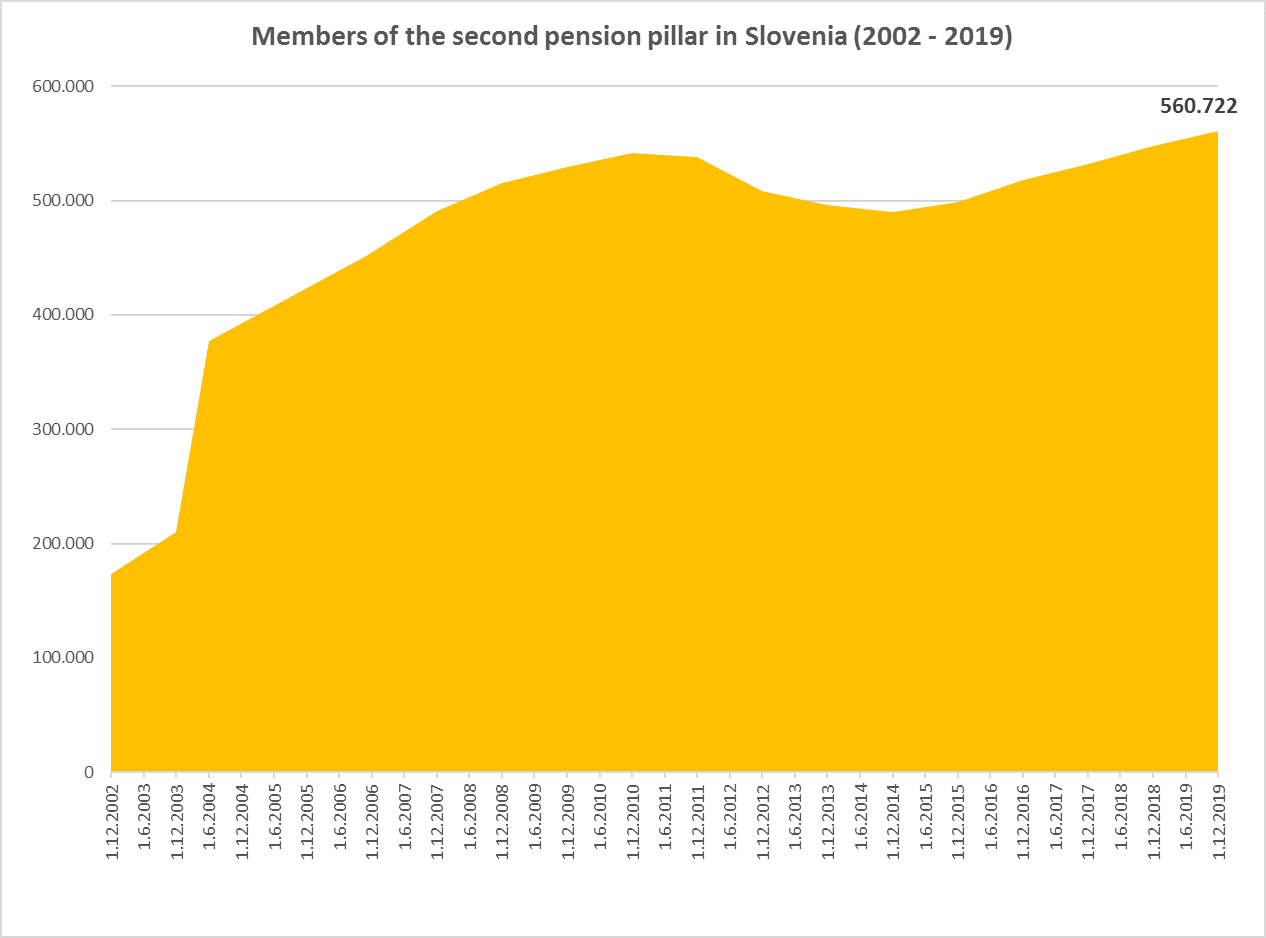

Existing from 2001, the second pension pillar in Slovenia is represented by private defined contribution retirement plans managed by specialised pension funds and insurance companies. The number of members has been steadily growing and at the end of last year reached 560.722 members, which is the highest number ever. This means the coverage rate is roughly 62 % of all persons in employment, which is a fairly decent rate for a voluntary system. But if we take away members of the civil servants mandatory retirement plan (approx. 235.000) the coverage rate drops to a more sobering 36 %.

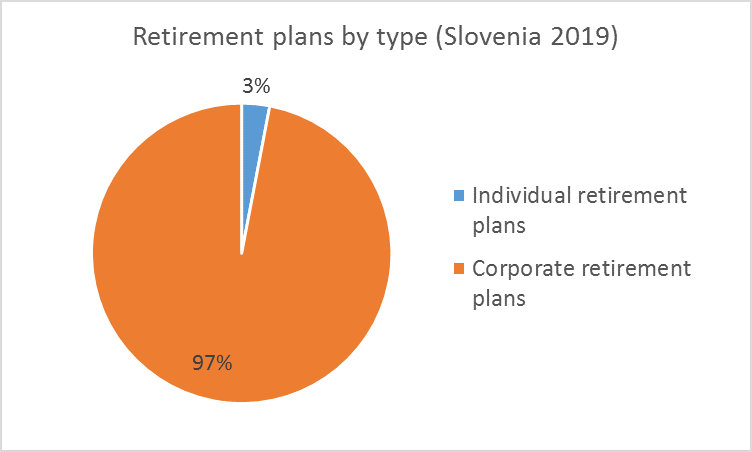

One interesting statistics exposes nicely the power of behavioral biases working against individuals to start saving for retirement, as the vast majority of the second pension pillar members in Slovenia (97%), are enrolled in corporate pension plans financed by their employers and only 3% of members save individually, despite the government’s tax incentives.

This percentage has been the same for 19 years proving jet agin, tax incentives for retirement saving have a very limited effect and only a very small percentage of employees decide on their own (not by their employer) to start saving for retirement. You can read more on why tax incentives for retirement saving don`t work in my previous blog post.

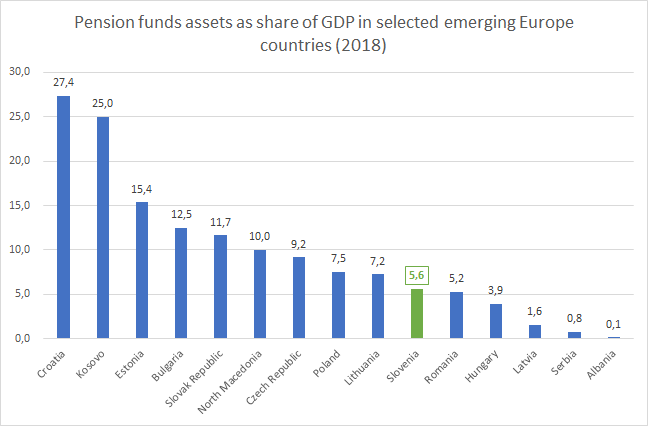

Total assets of pension funds also recorded steady growth and reached 2,62 billion Euros, representing a 12% growth from 2018. Despite the relatively large growth, assets of pension funds as a percentage of GDP remain at around 5% which is low compared to some other emerging Europe countries, as is evident from the chart below based on OECD statistics. The main factor influencing the growth of private retirement assets was the original design of the system and how members were enrolled. In countries like Croatia, Kosovo and Estonia, large assets are mainly thanks to mandatory enrolment in private retirement plans.

After 19 years we can say the second pension pillar in Slovenia reached average coverage rates for a voluntary retirement system and even that is mainly thanks to employer sponsored corporate plans. Tax incentives proved, as in many similar cases, ineffective to generate individual retirement savings. The main challenges for the future remain, how to increase enrolment and contribution rates in order to provide adequate income in retirement for the majority of future retirees, which will be more and more dependent on private pensions.

Where to go next?

Automatic enrollment in retirement plans is a great example of behavioral economics in action, where workers are defaulted into saving, but can always opt out. The United Kingdom is a great example of a successful implementation and employees were automatically enrolled in retirement plans from 2012 onward (first big companies, then medium and down to small), and to date it has helped over 10 million people to start additionally saving for retirement. After 8 years the coverage rate of retirement plans increased from 60 % to 90 % making it a great success. They did not stop at just auto-enrolment, but also contributions of members are auto escalated over the years making sure members will have sufficient assets at retirement. You can find more info on UK`s auto enrolment and the behavioral science behind it in the recent report from Nest Insight.

Ireland is following and plans to implement by 2022 a defined contribution auto enrolment system of supplementary pension savings for all employees between the ages of 23 and 60 who earn €20,000 or more. Auto enrolment will be phased-in and minimum mandatory contributions will be set at 1.5% of gross earnings and then increasing by 1.5% every three years until year 10, when they will reach 6%. The detailed legislation is still being drafted but you can find some more information on the plans in the report by Mercer.

Some US states, like California, Oregon and Illinois, are also following the lead with implementations of state-sponsored retirement savings plans in which employees are automatically enrolled. Oregon’s plan OregonSaves began in 2017, Illinois in 2018 and California started its CalSavers at the end of 2018. What is even better, more and more states are following their lead and the existing plans proved very resilient even to the latest COVID-19 crisis.

Auto enrolment in retirement plans and then auto escalation of contributions proved as a wining combination and I see no reason, why we should not learn from their experiences also in Slovenia and implement the proven lessons from behavioral economics to our retirement plans to increase coverage and assets and by that securing a brighter future for our citizens. With more and more strain on the public first pillar, additional revenue from private retirement plans will in the future not be any more a luxury, but a necessity.