According to the article in July’s issue of The Journal of Superannuation Management, you needed a tertiary level education* to understand or accurately interpret documentation related to your retirement plan. Guess how many Australians have a tertiary level education? Only 1,2 % of adults, hence the title of the article, Houston, we have a problem.

The background to the article above is, the company Ethos CRS reviewed the documentation comprising of product disclosure statements, financial services guides, annual reports and company policies of the 20 largest Australian superannuation funds (10 largest industry funds and 10 largest retail funds) and checked their documentation using their readability benchmarks comprising of the usage of active voice, average sentence length, readability score and grade level benchmarks (more details on this in the article) [1]. This gave them a quantifiable measure of the clarity and quality of each document and by doing this they could rank individual documents and also assess what kind of education level a person would need in order to understand or accurately interpret them. So to sum it up, you need to be pretty educated to understand all of the documents from your pension plan and I dare to speculate the needed education would be the same to understand documentation from Slovene or US pension plans.

Given the importance of retirement saving to the quality of an individual’s life in retirement, decisions about it – where to invest, how much to contribute, how to draw it down, are very important and one would ideally think that one of the things improving people’s decisions when it come to retirement planning would also be, how easily it is to read what funds put to members in writing online and offline. And let`s for a second ignore all of the behavioral biases influencing retirement planning decisions we dissect usually on our blog and the fact most people aren’t even remotely interested to read the investment policy of their retirement plan.

So why did the retirement plan documents score low on the readability benchmarks? Well for one, we are talking in most cases about long and complex documents (I work for a Slovene pension plan, so I know this pretty well), covering topics like investment policies of individual investment funds, risk mitigation techniques, … which are not really topics most people are familiar with nor interested in. Retirement plans are one of the most highly regulated areas of financial services in most countries meaning legislators and regulators prescribe in the smallest details what documents plans need to present to members and what those documents must contain. When you type all of it together, it comes in the case of the pension fund I work for in Slovenia down to 18 sheets of A4 paper written on both sides and this includes mandatory documents, like the individual pension plan rules, investment policy and key information document for each investment fund. All of it is mandatory and the scope of it is getting even bigger every few years as the European Union legislation is bringing new and new amendments to the local regulation (GDPR, IORP II directives, …) thus, increasing the volume of pension plan documentation even further.

So when a new member is enrolled in the pension plan, we must send to him or her by registered mail (email can be used, if the member gave the fund his email address and legal consent) all of the documents along with a cover letter informing him or her that their employer enrolled them in the pension plan. We don’t really need a study or a research paper to know most members get scared off by the sheer volume of papers which, even if they are written with the best intent to keep it simple, contain many words that fall in the financial or legal jargon, so the documents usually end up in the bin or a drawer without being read. From what we can gather from the Australian study, even if someone were to actually sit and start reading them, the information would be really tough for them to understand. So we are caught in a vicious circle, where legislators try to protect members by mandating pension plans to include more and more information and disclosures in their documents to help them make informed decisions about their retirement planning. What is forgotten in most cases, that by increasing the volume we are scaring away people and less and less of them read the documents, let alone understand them.

Luckily for us all, slowly a shift is coming at least in some countries, like the UK for one, and policy makers are drafting more and more behaviorally informed policies. This means the awareness is slowly here, that we will not protect or inform consumers purely by providing them more and more information and that new policies must be developed that take into account the phenomenon called information overload and the actual behavior of people and various behavioral biases and heuristics that influence it and are also the main focus of my blog in relation to retirement planning. Policy makers are, at least in some cases, starting to understand people will not start saving for retirement, if we only tell them that this is a prudent thing and they should do it. People will not stop using plastic bags or use more public transport purely because they all of a sudden started to worry about the environment and so on. Also organisations like the Behavioural Insights Team, that started in the UK with just a few people and has grown now to a global social purpose company or the Organisation for Economic Co-operation and Development (OECD) have all started digging in this field and came up with various recommendations for different behaviorally informed public policies.

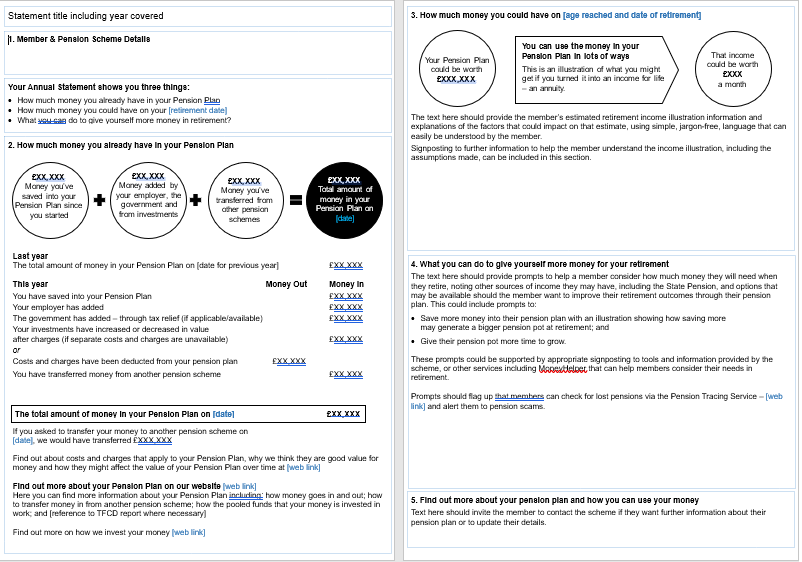

So what do they recommend regarding pension plan communication? Most recommendations go in a way of simplifying and standardising documents, for example entry forms or key information documents (KID), which members need to get before enrolling in the plans and annual benefits statements all members get once per year. In the UK The Department for Work and Pensions (DWP) published in 2021 a statutory guidance for simpler annual pension benefit statements that also contains a template for a one double-sided sheet of size A4 statement all providers can use and contains all of the key information a member should receive annually plus information where they can get more details if they wish for. The template shown below also has the exact wording that should be used in order to be as readable as possible and provide the appropriate information to members [2].

Illustrative template – Simpler annual benefit statement

Source: The Department for Work and Pensions (2021), https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1025143/illustrative-template-simpler-annual-pension-benefit-statement.odt

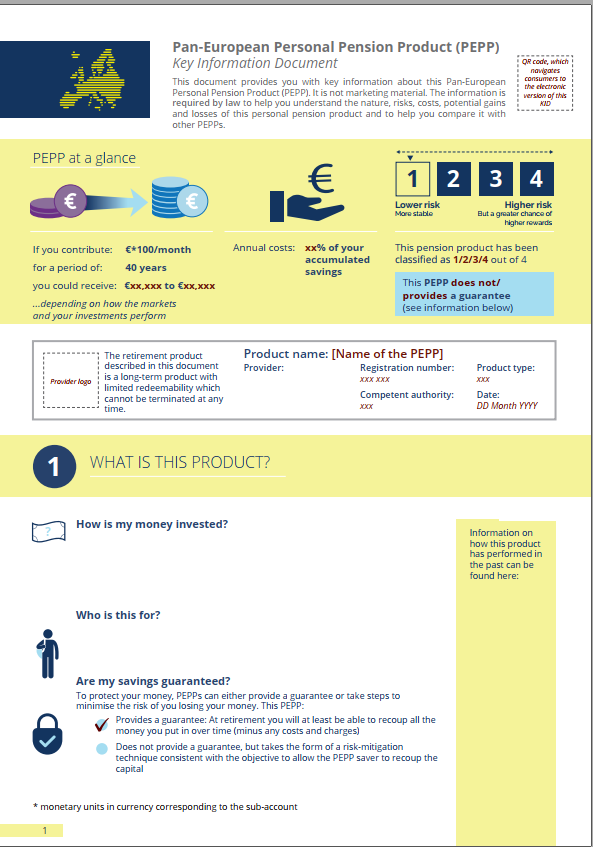

The European Insurance and Occupational Pensions Authority (EIOPA) is also pursuing a similar way with just published legislation for the new pan-European Personal Pension Product (PEPP) prescribing both the content, format and presentation of the key information document (KID) potential members receive before enrolling in the plan and also the PEPP Benefit Statement members they will receive once they start saving. The legislation makes it also cler, jargon needs to be avoided in these key documents and the font and size must be such that the information is “noticeable, understandable and presented in a clearly legible format”. The KID also needs to answer questions like “What is this product?”, “What are the risks and what could I get in return?” and “What are the costs?”. Similar as in the UK templates are also available and the design of them was publicly debated in consultations to achieve the best results [3].

PEPP KID Template

Source: EIOPA, https://www.eiopa.europa.eu/document-library/other-documents/pepp-benefits-statement-and-key-information-document-kid-template_en

All documents must be clear in both online and offline form and the legislation also encourages the layering of information which is another key feature we can implement to make retirement plan documentation more readable. Layering means that we do not present all of the content at once, but spread it on multiple layers and by doing this we avoid information overload and do not scare away people with long texts in the beginning, but provide at first only basic information and enable for only those who wish more content on additional layers. This is of course much easier in a digital environment, where additional information can be obtained with pop-ups and other similar features.

So to make retirement plan documentation easier to understand, we must first accept that just keeping it nice and short is due to legislation not always possible, but what is possible is, to provide basic documents like the key information document containing just the basic information new savers should receive before starting and once people are enrolled they should receive simple annual benefits statements. Both documents should be standardised so members get the same information with all providers in a certain country or even wider like the European Union, also enabling comparison between providers. Layering should also be used to avoid information overload and from the beginning legislators must adopt a digital first concept taking into account documents will be first in digital form, but can also be printed if needed.

Communication and engagement with members of pension plans is not only about sending them documents and there are many more channels of communications of course, with digital communications as the front runners for the future. This can be anything from just storing documents and delivering them electronically, having simple online accounts where members can see their balance, to much much more, like having personalised interactive communication with members with the use of smart chatbots or using elements of gamification to relay complex information in a simple, fun and engaging way. For one example of how I implemented gamification to communicate adequacy of contribution levels of individual members, you can check my post on LinkedIn from a few years ago and in one of the future articles on my blog I will explore the potential of information technology to enhance communication and engagement with members of retirement plans.

For now the key, when it comes to retirement plan documentation, is to keep it as simple as possible, if not use standardised documents that provide only key information to members and layer the information as much as possible to avoid information overload. Policy makers can make a real positive impact here with proper legislation and guidelines.

*According to The World bank tertiary education refers to all formal post-secondary education, including public and private universities, colleges, technical training institutes, and vocational schools.

References:

[1] Ethan, H. (2021). Readability scorecard for Australian superannuation funds. The Journal of Superannuation Management, volume 14, issue 3.

https://www.fssuper.com.au/article/2021-readability-scorecard-for-australian-superannuation-funds

[2] The Department for Work and Pensions (2021). Statutory guidance for simpler annual pension benefit statements.

[3] Commission Delegated Regulation (EU) 2021/473 of 18 December 2020 supplementing Regulation (EU) 2019/1238 of the European Parliament and of the Council with regard to regulatory technical standards specifying the requirements on information documents, on the costs and fees included in the cost cap and on risk-mitigation techniques for the pan-European Personal Pension Product (Text with EEA relevance)

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2019.198.01.0001.01.ENG