We all remember the roller coaster ride stock markets had in the year 2020 that started in march with a sharp drop in stocks of almost all sectors and industries, followed by equally or even higher rises of some industries in the later months of the year. All in all, most of the markets recovered by the year’s end and the S&P 500 finished in green with an annual total return of 18,4 %. If even professional traders were taken aback by last year’s volatility, the obvious question to be asked is, how did members of pension plans, represented mostly by ordinary employees, react to the volatility? Did they panic and switch funds from more dynamic to conservative, vice versa, or did they do nothing and hold their ground?

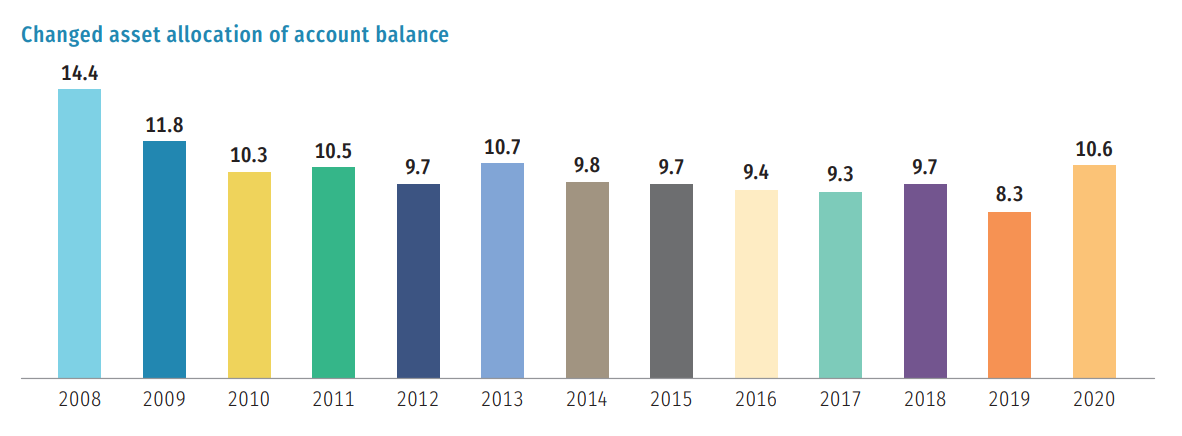

Few studies on this very topic were published in the last days and all tell a similar story. The Investment Company Institute (ICI) report establishes that most members of defined contributions retirement plans in the US stayed the course with their asset allocations despite high market volatility. The report states 10,6 % of DC plan members changed the asset allocation of their account balances in 2020, which is a bit more than 8,3 % in 2019, but lower than 11,8 % in 2009, as the stock market started to recover from the global financial crisis. The data for the report came from ICI’s survey of a cross section of recordkeeping firms representing a broad range of DC plans and covering more than 30 million employer-based DC retirement plan participant accounts. The report also provides a nice historical comparison of what percentage of members changed their account balance asset allocation from the year 2008 to 2020, shown below [1].

Source: ICI Survey of DC Plan Recordkeepers (2008–2020)

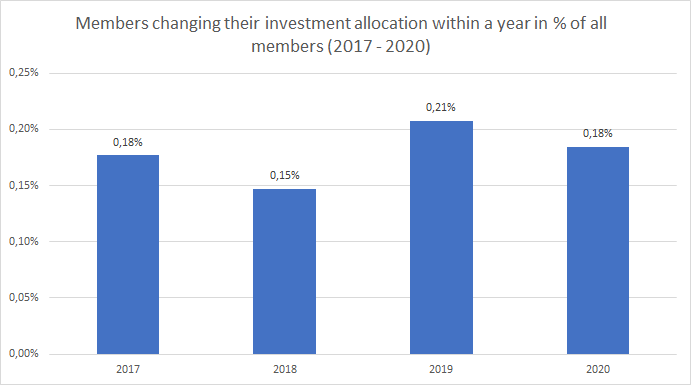

To check if the same pattern would also be found on the other side of the Atlantic, I did a short analysis of how many members changed their account balance asset allocation of Pokojninska družba A, Inc. pension fund where I work, which is a private DC pension plan from Slovenia with 51.500 members end of 2021. Members in our fund can choose between three life cycle funds, ranging from the Equity fund, with obviously high equity exposure, to the Balanced fund with medium equity exposure and the most conservative Guaranteed fund, with 80% bond allocation and capital guarantee. As is evident from the chart below, showing what percentage of members switch their investment allocation annually, the average numbers are much much lower than in the US. In fact even less than 0,5 % of members annually change their asset allocation and 2020 was no exception.

Even though I did not expect high numbers of members to change their asset allocation in the last year, I was really surprised at how low the numbers really were. Only 0,18% of all members changed their asset allocation in 2020, which is a bit less than in the year 2019 and basically on the average of the last four years. If we look from which fund members were switching out the most and adjust the numbers to represent how many members are in each fund, then most changes of allocation were done from the Equity fund to one of the more conservative funds.

If we dig further and look at the monthly levels we can see most members in our funds change their asset allocation in the first quarter of the year. There are probably many reasons for this seasonality, one for sure being all members receive at the end of January their annual account balance statement in which they also see the funds performance for the last year and that can stimulate some movement. We saw most changes to the asset allocation in the first few months of the year 2019 where members saw the equity fund achieved a negative yield in 2018 and that could scare a few members to change their allocation to the conservative guaranteed fund which recorded a positive yield.

The difference in the percentage of how many members change their asset allocation annually in Slovenia and the US is huge, but some of the reasons for it make it not so surprising. In Slovenia pension funds started to offer life cycle funds only from 2016 onwards, before the legislation did not unable fund selection and the only option was the guaranteed fund, so people even today are not so much aware of the investment options as are savers in US pension plans which have for long had a much wider fund selection.

So to answer the question from the beginning of the article, did the stock market volatility in 2020 affect asset allocation of pension plan members? The answer is short, no. The majority of members held their ground and did nothing which is good, as we all know changing asset allocation in panic results in most cases in suboptimal performance, to put it mildly and Morningstar had a nice article on why investors should stay the course throughout market turmoils [2]. One thing that we also need to keep in mind, most members of pension plans contribute to their accounts on a monthly basis and that evens out fluctuations in the members balances. So If you are checking online your account balance the monthly contributions make it tougher to see how much the value of your assets went up or down in a certain month which is good, as there is not much good from being fixated on monthly fluctuations if you are saving for the long run, which saving for your retirement for sure is.

References:

[1] Holden, Sarah, Daniel Schrass, and Elena Barone Chism. 2021. Defined Contribution Plan Participants’ Activities, 2020. ICI Research Report (February). Available at http://www.ici.org/pdf/20_rpt_recsurveyq4.pdf

[2] Lauricella, Tom. 3 Charts That Show Why Investors Should Stay the Course Throughout Market Turmoil, 2020. Morningstar, Inc. Available at https://www.morningstar.com/articles/972119/3-charts-that-show-why-investors-should-stay-the-course-throughout-market-turmoil