Since the Slovenian ministry of labour just released fresh stats for the second pension pillar, this just calls for an updated article on the evolution of the second pension pillar represented by defined contribution retirement plans.

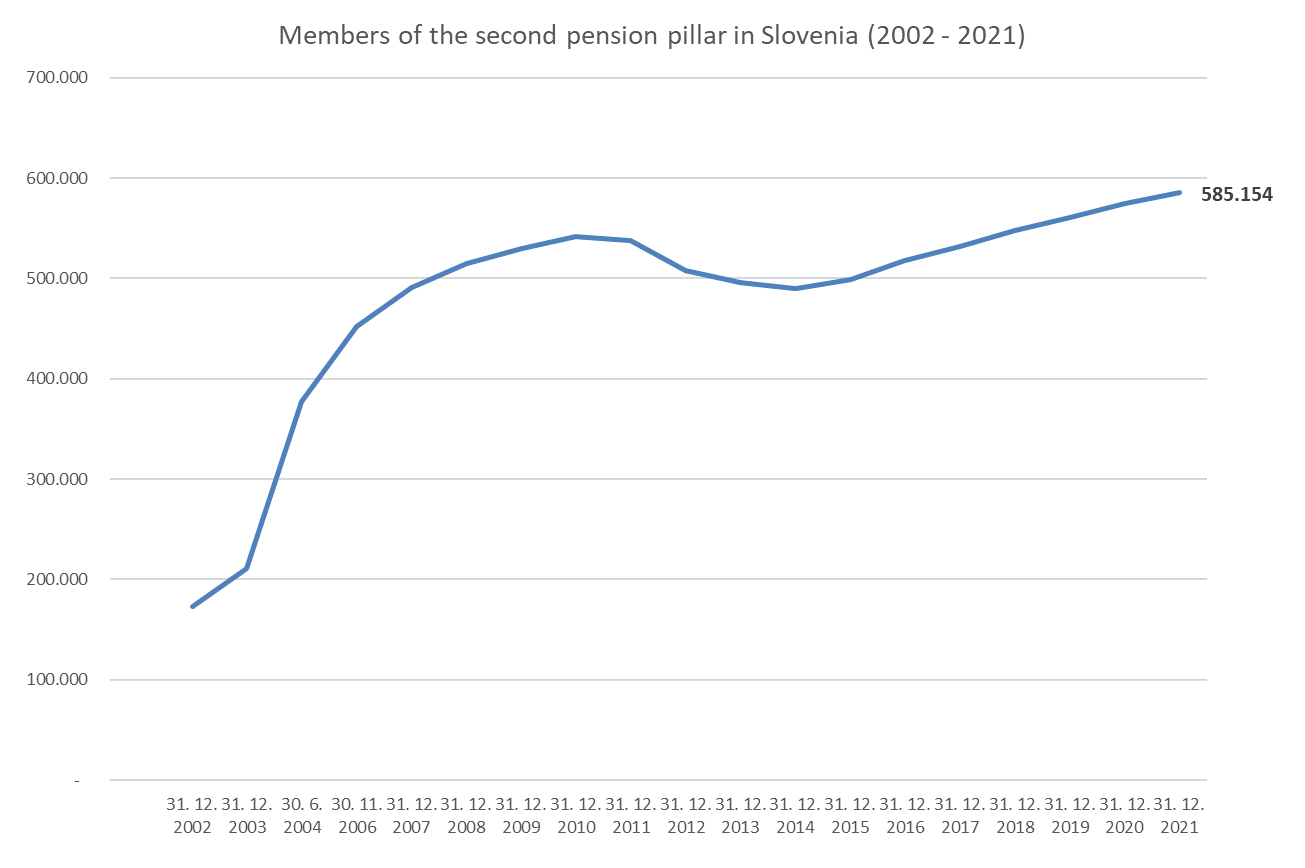

In December 2021 the number of employees saving in the second pension pillar in Slovenia reached a record 585.154 members, representing a 1,9% increase from the last year. The growth rate is quite disappointing, since the growth rate is almost identical to the growth rate of employed persons. This means the growth of members came predominantly from the increased employment in companies, which already have collective pension plans, and not from companies starting new pension plans or from individuals deciding to start saving on their own.

The coverage rate of pension plans is 59,9 % of all persons in employment, which you would say is a fairly decent rate for a 21 year old voluntary pension saving system, but if we deduct from this the number of civil servants, who are enrolled in a special mandatory retirement plan (approx 245.500), the coverage rate drops to a more realistic 35% of all persons in employment, which is the same as last year. Also worth pointing out, the vast majority of members (94 %) are enrolled in collective pension plans financed by employers, so jet again backing up the age old argument, that individuals very rarely save on their own for retirement, because of the many behavioral biases plaguing this decision and some also because of structural (economical) reasons.

All this confirms my views expressed in previous articles, that unless we implement necessary reforms of the pension system by introducing mandatory auto enrollment in pension plans, the coverage rates will not increase on its own and will stay under 40 %. And all the financial education in the world and tax incentives for retirement saving will not change this. Of course they are important, but they will not change the existing state noticeably (more on how financial incentives have a very limited effect on retirement saving in my article from 2020).

If we continue the updated review of the second pension pillar in Slovenia, assets of pension funds increased to 3,06 billion euros by the end of 2021 which represents a 9 % annual increase. Assets of pension funds as a percentage of GDP are at around 6%, which is low compared to some other emerging European countries, like neighbouring Croatia, where assets of retirement plans are closer to 30 % of GDP. Croatia chose in 2000 a different path than Slovenia and implemented mandatory enrollment in the second pension pillar, which clearly shows to be the better choice now, as both coverage rates and assets of pension funds far exceed the ones in Slovenia. More detailed comparison of the two models of retirement plans and their success in my article from last year.

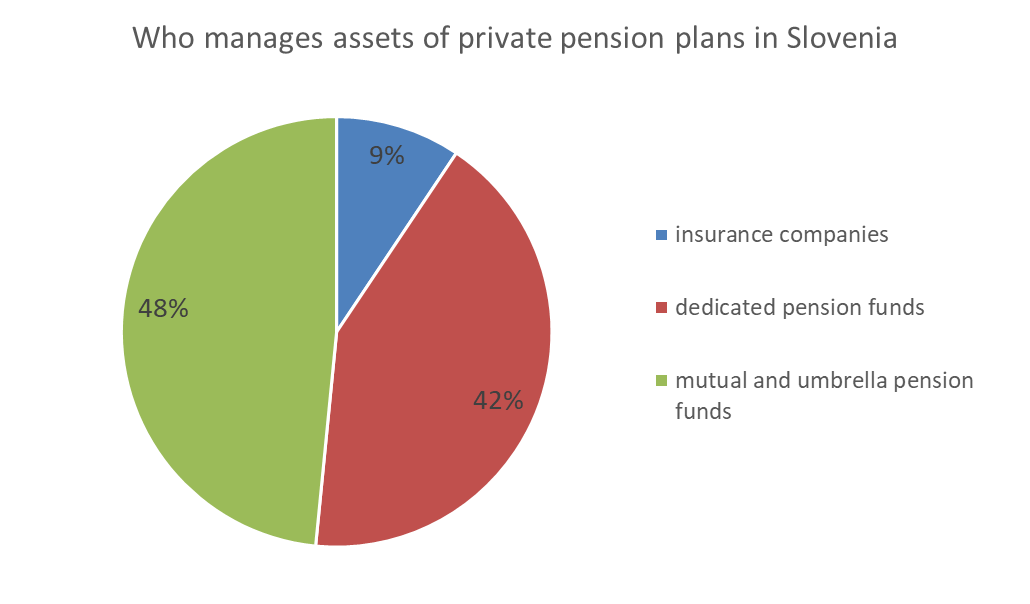

Pension plans in Slovenia can be managed by dedicated pension funds, insurance companies or mutual and umbrella pension funds and you can see the breakdown of the market in the chart below.

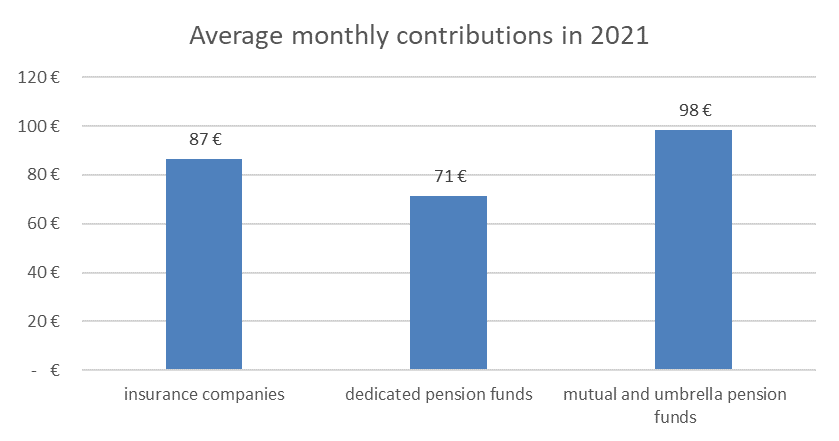

Average monthly contributions were 87 € for members of pension plans managed by insurance companies, 71 € for dedicated pension funds and 98 € for mutual and umbrella pension funds (not counting contributions to the mandatory plan for civil servants). This means monthly contributions were in the range of 4,4 % of the average monthly gross salary for insurance companies, 3,6 % for dedicated pension funds and 5 % for mutual and umbrella pension funds, which is not great, not terrible, if i borrow the words of Anatoly Dyatlov from the Chernobyl TV series.

Benefits of the second pension pillar

Keeping in mind private pension plans in Slovenia exist now for only 21 years, the numbers of members receiving annuities is fairly limited and is currently just below 50.000 and official statistics on them are fairly limited. Regarding decumualtion options for private pension plans in Slovenia, under current rules, for collective plans life annuities are the only possible option (only exception if assets at retirement are below 5.000 €, they can be paid out as a lump sum), for members of individual pension plans they can choose between lump sum payout or one of the life annuities on offer.

From first hand experience (I work for one of the largest pension funds) I can say the members that start to receive annuities are our best “promoters”, as they confirm to all other employees that they actually receive an additional income thanks to their participation in the private pension funds. This is still, after 21 years, the biggest concern most members have, will we receive something in the end, and this is massively improving in the last years, when more and more members are starting to receive benefits. Also worth noting is the success of life cycle funds, which were introduced only in 2016 and from that point on members can choose between three investment funds, and the younger members can also have their assets invested in high equity exposure funds that invest globally and this choice was lacking before.

Returning to the point already made in the article, from all the behavioral science literature out there, and there is a lot, and also hard data from other countries, I’m quite certain that unless we follow countries like the UK, and Ireland recently, and implement policies requiring all employers to mandatory auto enroll their employees in retirement plans, we will never get past the 40 % coverage rates and the second pension pillar will in Slovenia continue to play a marginal role at securing additional income to retirees, which will be more and more needed, as first pillar pensions will continue to decline, meaning retirees will need additional streams of income to supplement this in order to live a decent life in retirement everyone deserves after 40+ years of work. For more insights on how auto enrollment was introduced in the UK and what was the genius thinking behind it, you can listen to the latest episode of The accidental plan sponsor podcast, which really nicely reveals how this interesting policy change came to life.

To borrow Einstein’s words, “The definition of insanity is doing the same thing over and over again, but expecting different results.” so we really need to grasp this in Slovenia. Unless changes are made, the second pension pillar will have no more than 40 % coverage rate, the third pension pillar is almost non-existent, leaving heavy reliance on first pillar pensions alone. Given the massive demographic shift already underway in Europe decreasing the sustainability of first pillar systems, relying only on one stream of retirement income is not a prudent solution, to put it mildly, and we should strive to have multiple sources of retirement income to live as comfortably as possible.

A new government is just forming in Slovenia in the days of me writing this article and I sure do hope one of the first things they will tackle is the evolution of the pension system and we will follow proven examples from the likes of the UK, that managed to increase coverage rates drastically by introducing auto enrollment in retirement plans.

References:

Ministry of Labour, Family, Social Affairs and Equal Opportunities (2022). Statistic for supplemental pension insurance. Retrieved from: https://www.gov.si/teme/prostovoljno-dodatno-pokojninsko-zavarovanje/

Vižintin, Ž. (2020). Tax incentives for retirement saving don`t work (what does?). Irrational Retirement Blog. Retrieved from: https://irrationalretirement.com/2020/07/17/tax-incentives-for-retirement-saving-dont-work-what-does/